When borrowers first hear about federal student loan consolidation, they often think of it as a technical financial move rather than an opportunity to reshape how they manage their loans. But consolidation can offer far more than a single payment each month. It can create a sense of structure and predictability that may have been missing for years. When viewed as a way to simplify not just payments but also decision making, consolidation can become a valuable tool for long term financial confidence. This is why many people exploring their options for student loan consolidation choose to look beyond the basics and consider how consolidation fits into their overall financial strategy.

Streamlining the Complexities

For many borrowers, student loans are not overwhelming solely because of the balance. The complexity of multiple due dates, varying interest rates, and different servicers often contributes just as much stress as the debt itself. Consolidation streamlines these moving parts into a single loan with one servicer and one monthly payment. This reduces the mental burden and helps borrowers stay consistent with repayment. It also becomes easier to predict how the loan will behave over time since the repayment schedule becomes uniform instead of scattered.

Another helpful perspective is recognizing that consolidation is not about reducing debt instantly. Instead, it creates a structure that allows borrowers to manage their loan obligations more sustainably. This shift from short-term thinking to long term planning helps individuals choose repayment strategies that reflect their financial goals, whether those goals involve lowering monthly payments, qualifying for forgiveness programs, or preparing for future milestones like homeownership.

What Federal Student Loan Consolidation Actually Does

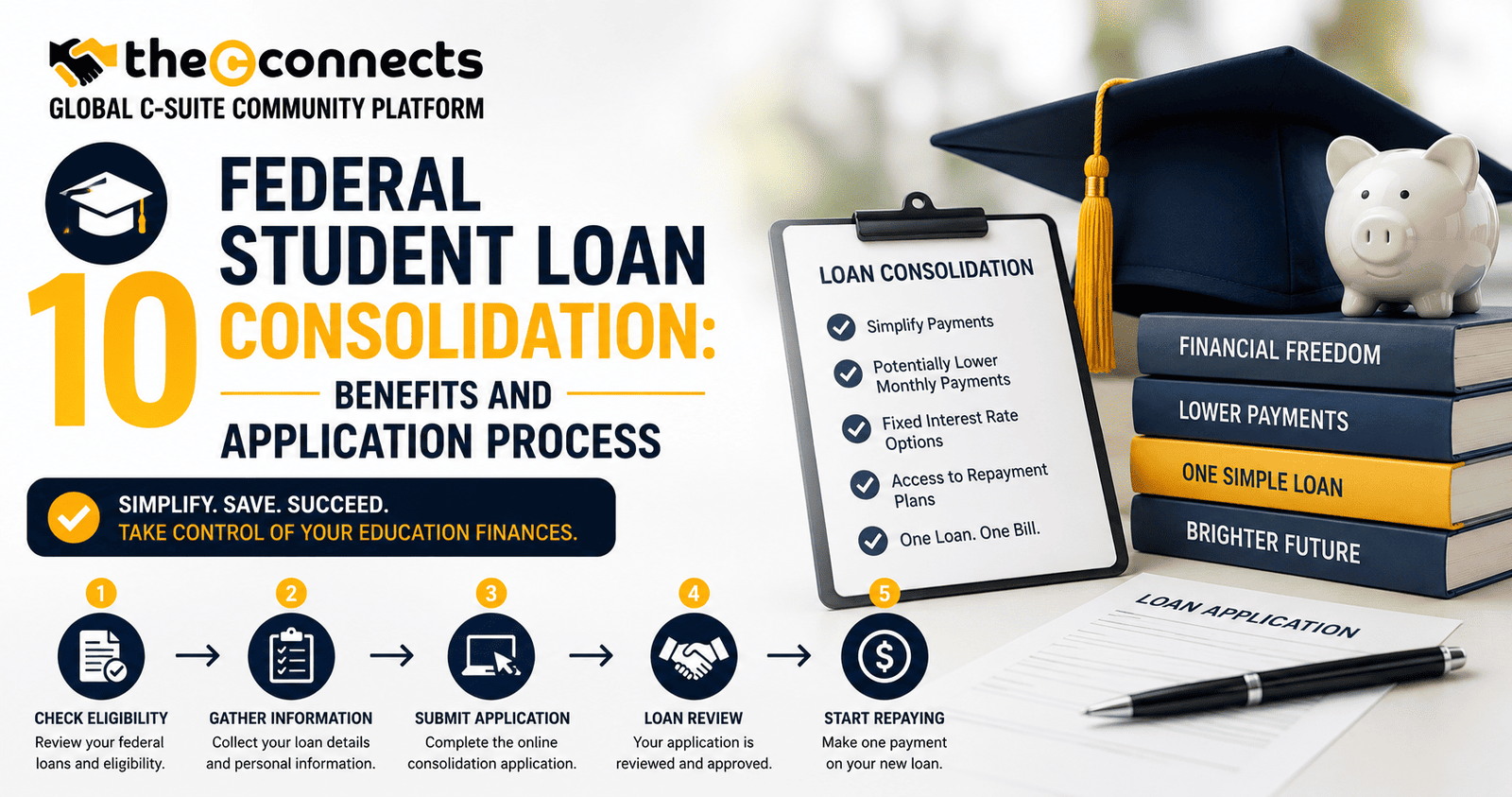

Consolidation through the federal government combines multiple eligible federal student loans into a single Direct Consolidation Loan. This new loan has a fixed interest rate based on the weighted average of the interest rates from the original loans. Although the rate will not decrease significantly, consolidation ensures predictability by locking the rate in for the life of the loan.

Borrowers may also gain access to additional repayment options offered through federal programs. For example, some income driven repayment plans require a Direct Loan to qualify. Consolidation can make a borrower eligible for these programs, which can be especially valuable during times of financial transition.

Another benefit is the ability to move loans out of default. Consolidation can offer a clean slate for borrowers who have struggled to stay on track. By consolidating and agreeing to an appropriate repayment plan, borrowers can regain access to federal protections and bring their loans back into good standing.

Key Benefits That Borrowers Often Overlook

Many people know consolidation simplifies loan repayment, but there are additional advantages that are less commonly discussed. One of these is the potential to tailor repayment timelines. Federal consolidation often allows borrowers to extend repayment terms, which lowers monthly payments and increases breathing room in the budget.

This does come with the tradeoff of paying more interest over time, but for borrowers experiencing financial strain, the immediate relief can be greatly beneficial. It may also prevent missed payments and protect credit scores, which can be especially important during periods of job loss or major life changes.

Another benefit is organizational clarity. With a single loan servicer, borrowers have a centralized place to access statements, make payments, and request assistance. This consistency can reduce administrative mistakes and make it easier to track progress.

Eligibility Requirements and Loan Types

Not all federal loans need consolidation, but many can be included. Eligible loans generally include Direct Loans, Federal Family Education Loans, Perkins Loans, and certain types of parent loans. The application is free and handled through the federal government, so borrowers should avoid any company that charges unnecessary fees for assistance.

The United States Department of Education offers detailed guidance on which loans qualify and how the process works through its official resource on federal student loan consolidation and repayment options. Reviewing this information is an excellent way to ensure you are choosing the most suitable path.

How the Application Process Works

Applying for federal student loan consolidation is relatively straightforward. Borrowers complete the process online by selecting which loans to consolidate and choosing a repayment plan. The application allows borrowers to view available repayment options based on income and loan type.

Once submitted, the consolidation process typically takes several weeks. During this time, borrowers can continue to make payments to avoid interest accumulation or delinquency. When the new loan is finalized, the borrower begins making payments under the selected repayment plan.

One important detail is that consolidation resets certain timelines. For example, those pursuing Public Service Loan Forgiveness need to be aware that consolidation may restart the qualifying payment count unless it is done before entering a forgiveness program.

Income Driven Repayment and Forgiveness Opportunities

One major advantage of consolidation is gaining access to income driven repayment plans. These plans base payments on household income and family size, making it easier for borrowers to manage monthly obligations during financial hardship. Some plans also include forgiveness after a set number of qualifying payments.

Forgiveness options vary, and understanding the eligibility rules can be complex. Reliable resources such as the Federal Student Aid website and the Consumer Financial Protection Bureau’s resource on repayment assistance and borrower protections can help borrowers determine which programs they qualify for.

Common Misunderstandings About Consolidation

Consolidation is often confused with refinancing, but the two are different. Federal consolidation remains within the federal system, preserving access to protections such as income driven repayment, deferment, and forgiveness. Refinancing involves transferring loans to a private lender, which may offer a lower interest rate but eliminates federal benefits.

Another misunderstanding is the belief that consolidation automatically lowers interest rates. While it can simplify repayment and open new doors, reduction in interest is not the primary purpose. The focus is on long term manageability and flexibility.

Final Thoughts

Federal student loan consolidation offers a powerful way to simplify repayment, access more flexible payment options, and create a clearer financial path forward. Whether you are struggling to keep track of multiple loans or looking for a more structured repayment plan, consolidation can help reduce stress and support long term success. By understanding how the process works and evaluating your financial goals, you can choose an approach that provides stability, clarity, and momentum for the years ahead.

Contact TheCconnects

📧 Email: contact@thecconnects.com

📞 Phone: +91 91331 10730

💬 WhatsApp: https://wa.me/919133110730